Welcome to Salary Series! I am asking real people what they make, what they do, and how they spend their money. If you are interested in submitting your information, you can do so here.

Profile:

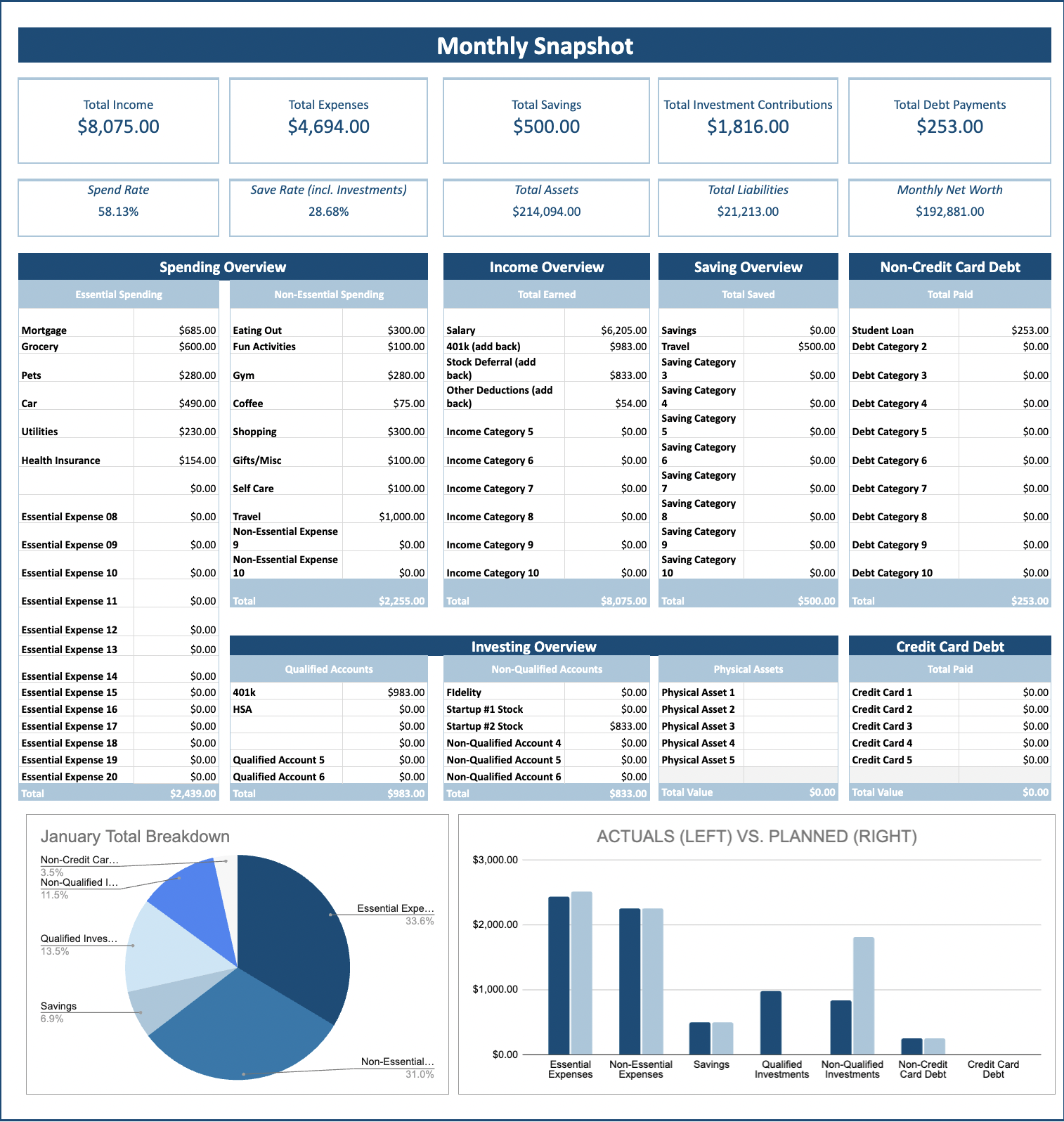

Job Title: Director of Regulatory Affairs

Industry: MedTech Startup

Location: Durham, NC

Annual Salary: $128,000

Bonus: $38,400 Annually

Side Hustle: Approx. $500 per month consulting for another startup

Education: Georgia Tech – B.S. in Biomedical Engineering, 2020

Financial Profile:

Essentials:

Mortgage: $865 (her half)

Groceries: $600

Pet: $280

Car/Gas: $490

Utilities: $230

Insurance: $154

Non-Essentials:

Dining out: $300

Fun Activities: $100

Gym: $280

Coffee: $75

Shopping: $300

Gifts/Misc: $100

Selfcare (nails/hair): $100

Travel: $1,000

Financial Goals:

401k: $983

HSA: $54

Stock Deferral: $833

HYSA (Travel): $500

Student Loan: $253

Assets

HYSA: $9,682

HSA: $348

Investments (Fidelity): $12,143

Startup #1 Stock: $53,930

Startup #2 Stock: $121,537

401k: $16,454

Debts

Mortgage: $$314,925 (30-year, 2.85%)

Student Loans: $21,213 (variable 4.5-5.75%)

Net Worth

$192,881

(excluding mortgage since she did not provide her equity in the home)

Please provide any additional context around your financial situation that may be helpful.

I bought my house in 2021 and lived alone for 2 years. My boyfriend and I live together now and we split the costs for mortgage, utilities, groceries, and any home improvement. $833 per month goes to employee stock deferral so that I can pay into the company in hopes of our startup going public in the next 2-3 years. I largely prioritize this since it is the best opportunity for investment available to me right now and I can directly contribute to the success and outcome of that investment. It is not guaranteed money since there is no current market to be able to sell it as both start ups are privately held.

Currently saving to establish a travel fund to pull from. I love to travel and right now just budget monthly some travel, but it makes it hard to book things in advance to take advantage of good rates for things far out. I’m working to build a savings fund for travel so that I can better budget that money annually and know what I have to spend on travel for the upcoming year. Just opened a HYSA for this and would like to save $500/month there/$833 per month to company stock which is the main location of my investing currently/$253 per month goes to student loans for a 10 year pay off. I would like to prioritize larger chunks of payoff in the future since this is my highest interest rate debt.

Did you parents pay for college/ do they support your financially in any way?

Parents paid for some of college and I had a minor scholarship and inheritance. I have $21,213 remaining in student loans from the split of contribution to tuition and what I took out. They paid for my housing my first year, but then I worked and paid my rent and expenses for the remainder of college once they had 3 kids in college all at once. I also received $10,000 from my parents for contribution to my down payment for my house.

What tool(s) do you use to manage your money?

PFD!!! Just purchased it about 3 months ago and it has been so helpful in changing the way that I budget my money.

Do you feel confident in your finances?

Getting there, I find it really difficult to determine what to prioritize with my money. Debt payoff vs investment vs retirement. I still want to live and enjoy life but want to set myself up well for the future.

Do you feel like you are financially “behind” your peers? Why/why not?

For me money has been really taboo and I have not discussed it in detail with my peers. I would like to change this narrative and make it more normal and approachable so that we can all share tips. When looking at other peoples finances, especially in the world of personal finance social media, you see the extremes (or at least I think so) of those that are either doing really well, or those really struggling. It is hard to know who is the general population to even compare against.

What is your biggest money struggle?

Making informed decisions on where to put my money, and to not overindulge in material things or expensive travel to keep up with the people around me. It is easy to see what people show off (cars, clothes, travel, eating out at fancy restaurants) but it is not as easy to see what they are putting away for retirements, saving, etc. to be able to know you are spending your money wisely.

What financial goals are you working towards right now and why?

Building up a travel fund! Travel is really important to me and where I most like to spend my money. A savings account dedicated to this will greatly help me budget for this better.

Are you looking for tips/advice? If so, please ask your question here and I will do my best to answer. Make sure you provide as much info/context as possible!

Would you prioritize debt payoff (i.e., student loans) over putting money in investments, savings, etc.? Any areas of recommendation to cut down spending (gym is the only one that is a non-negotiable)?

Michela’s Advice: Just to start things off here – your financials are amazing. Your income is great, you are making money from your side hustle, you own your home, and it seems like you have a great grasp on your spending! Kudos!!

When it comes to prioritizing your goals, you have a few options. Based on what you provided, you have about $700 of unallocated money and that is not including your side hustle income or your bonus. Here is what you can consider:

-Get clear on how much you want to save for travel. At $500/month, that will put you at $6k annually. Is this enough for what you want to do? Adjust accordingly if needed.

-Use the PFD to amortize your loans and see when your debt payoff date would be. Given the rates are all still fairly on the lower side, adding more money to your loans is not necessary, but given you have the flexibility to do so, it may be worth considering an extra $100-$200 monthly, OR allocating side hustle income to this when you earn it.

-Given the majority of your non-retirement investments are in your startup, I’d consider diversifying your position outside of retirement and startup investments. You could continue adding to your Fidelity account in addition to the other investing you’re doing.

Ultimately, you are doing really well and you have the income flexibility to spend how you need and contribute over 30% towards your various goals. This is amazing!

Personal Finance Dashboard Monthly Snapshot